WHEN people think of a large Asian country on the brink of deflation, they probably have Japan in mind. But China, the biggest of them all, is now skirting close to outright falls in prices across a wide swathe of the economy. Producer prices have been declining for nearly three years and consumer price inflation is mired at its lowest level since 2010.

Deflation is rightly feared by central bankers around the world as a most destructive economic force, making debts more expensive in real terms and leading to a vicious cycle of contraction as consumers delay purchases and companies put off investments. Yet the Chinese central bank has been remarkably laid-back about the downward lilt in prices. The most obvious tool in its kit to arrest the slide would be to cut interest rates, but it has not done so since July 2012; the benchmark one-year lending rate remains lofty at 6%. What explains the central bank’s calm in the face of falling prices, and is it making a big mistake?

Inflation data published on Monday provide the latest evidence of China’s descent towards deflation. The consumer price index (CPI) rose 1.6% in October from a year earlier, the lowest since the start of 2010. Month-on-month CPI inflation was flat, falling back from September’s 0.5% increase. Core inflation, stripping out volatile food and energy prices, ticked down to 1.4% year-on-year in October, below the 1.7% average over the previous nine months. Meanwhile, the producer price index (PPI) ran deeper into negative territory. Prices of goods as they left factory gates fell 2.2% in October from a year earlier, steeper than the 1.8% decline in September. PPI has been in deflation for 32 straight months.

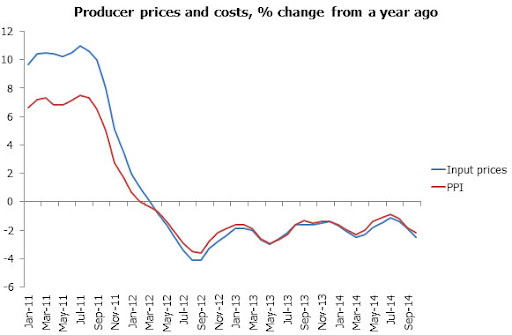

But not all episodes of deflation are created equal. Prolonged falls in prices would normally make an open-and-shut case for policy easing. In China, it is a little more complicated. The decline in PPI, which on the surface is the most alarming of the price trends, has been caused almost exclusively by the slump in global commodity prices. This can be seen in the near-perfect correlation between producers’ output prices and their input costs.

Lower costs have allowed companies to remain profitable even as their selling prices have fallen. Industrial profits slumped badly in 2012, when China’s economy dipped below 8% annual growth for the first time in more than a decade. Over the past two years, though, companies have gradually acclimatised to weaker growth, and profits have recovered. This trend is continuing: while producer prices fell 2.2% year-on-year in October, their input costs fell 2.5%.

On the consumer side, price trends are also less worrying when looked at in more detail. Headline CPI has come down from more than 6% at the end of 2011 to less than 2% now. That is well below the government’s target of 3.5%. But the lower CPI has stemmed from softer food inflation, a welcome development for China, as it is for most other developing countries. Prices for consumer goods, from household appliances to clothing and entertainment-related products, have been far steadier. What’s more, a tight labour market means that wages have kept on rising, a solid foundation for resilient consumption. Incomes in urban areas increased 9.3% in the first nine months of 2014 from a year earlier, growing faster than the overall economy.

So despite the apparent weakness in prices, deflation is simply not a big concern for China at present. Nevertheless, softer inflation does give the central bank more room to ease monetary policy. For Chinese companies labouring under the piles of debt that they have accumulated in recent years, lower interest rates would bring relief by reducing their refinancing costs. A growing number of economists, both Chinese and foreign, are now calling for the central bank to cut rates. One popular explanation for why it is reluctant to so is that it fears signalling a more aggressive easing than it actually intends. China’s top leaders, including Xi Jinping over the weekend, have repeatedly said that they want to focus on structural financial and fiscal reforms that will pay dividends in the long run. Rate cuts might be misconstrued as a short-term balm for the economy that runs counter to the reform agenda.

The central bank is not entirely sitting on its hands. Over the past two months, it has deployed a new medium-term lending facility to give banks almost 800 billion yuan ($130 billion), a cushion of liquidity for the economy that can be rolled over and, if needed, expanded. It has also guided lending rates lower via its open-market operations. These easing measures are subtle. But with deflation demons still at bay, China’s central bank need not be blunt.

No comments:

Post a Comment