A weak domestic economy is spurring Japanese firms to expand abroad Nov 1st 2014 |

Hun Sen is shopping, just like Japan Inc

IT IS not every day that the opening of a shopping centre attracts a prime minister, but then Aeon Mall in Phnom Penh is not any old shopping centre. The Japanese-built complex is Cambodia’s biggest, complete with an ice rink, television studio and bowling alley. For Hun Sen, the attending prime minister, it is a symbol of Japanese investment. Governments across South-East Asia are courting Japanese firms, and a torrent of yen is surging their way.

IT IS not every day that the opening of a shopping centre attracts a prime minister, but then Aeon Mall in Phnom Penh is not any old shopping centre. The Japanese-built complex is Cambodia’s biggest, complete with an ice rink, television studio and bowling alley. For Hun Sen, the attending prime minister, it is a symbol of Japanese investment. Governments across South-East Asia are courting Japanese firms, and a torrent of yen is surging their way.

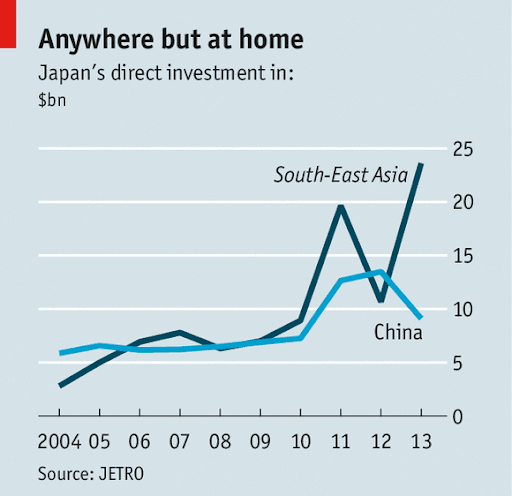

Japanese investment in the region doubled to 2.3 trillion yen ($24 billion) last year, the latest in a series of sizeable increases (see chart). Part of that is mergers and acquisitions by Japanese firms, which have skimped on investment at home and so have a cash hoard of some ¥229 trillion. SoftBank, a Japanese mobile carrier, just led a $100m investment in Tokopedia, an Indonesian e-commerce firm; Toshiba, a conglomerate, has pledged to invest $1 billion in South-East Asia over five years. A year ago Mitsubishi UFJ Financial Group, Japan’s biggest bank, spent ¥536 billion to buy 72% of Thailand’s Bank of Ayudhya.

During the first wave of Japanese investment, in the 1980s and 1990s, money poured into Thailand, Malaysia and Singapore, building up their automotive and electronics sectors. That flow largely ceased after the Asian financial crisis of 1997-98, when Japanese firms began to focus on China’s vast, cheap labour force.

Yet with labour costs now steadily rising in China, and political tensions between Japan and China continuing to flare, South-East Asia looks attractive again. Japanese investment in China fell by nearly two-fifths last year, even as it grew in places like Cambodia. Although China is still Japan’s biggest trading partner, Japanese firms invested nearly three times more in South-East Asia last year. For South-East Asian countries, too, Japan is an important hedge against China.

But the embrace of South-East Asia is not without its critics. Some worry that the headlong rush to the region by Japanese banks, in particular, may prove short-lived. In 2013 the Bank of Japan began buying bonds with newly created money (quantitative easing), as part of a plan by Shinzo Abe, the prime minister, to banish deflation and boost growth. The central bank’s purchases left Japanese banks with lots of cash: they keep roughly 15% of their assets as excess reserves at the BoJ, earning minuscule returns. Since demand for loans in Japan is still subdued, they are hunting for borrowers abroad. Lending by Japanese banks to the rest of Asia, including China, has grown quickly since the end of 2012 and stood at $465 billion in June. But if Japan’s monetary policy changes, such flows could reverse.

Meanwhile, Japan’s government wants local firms to invest more at home. Quantitative easing has weakened the yen, making it more attractive to do so. But Japan’s rapidly ageing population means the domestic market is shrinking, undermining the incentive to build new factories. For every Canon, a camera-maker, which recently said it would increase the share of its production in Japan, there are several counter-examples, such as Mitsubishi Motors, a carmaker, which is building a new factory in Indonesia. Japanese firms focus more on profits than in the past, thanks to improvements in corporate governance, notes Robert Feldman of Morgan Stanley, an investment bank; that is prompting them to look for better prospects abroad.

With more production shifting abroad, Japan’s exports are also suffering. Deutsche Bank estimates that outbound investment reduced Japan’s trade balance by as much as 16 trillion yen in 2012, by providing local substitutes for Japanese exports. That is more than Japan’s trade deficit that year of 7 trillion yen. Profits from abroad were not sufficient to make up for the damage to the current account. As overseas ventures accelerate, they will help tilt Japan towards a trade deficit more often, leaving its financial system more vulnerable to the fragilities built up over decades.

The risk is that Japan could become a “rentier” economy, says Martin Schulz of the Fujitsu Research Institute in Tokyo. In this scenario, Japanese firms do not make the investments in Japan that are needed to generate broad-based wage growth, and focus instead on their foreign ventures. That would leave Japan living off the “rent” from its foreign assets, rather than the fruits of domestic economic activity.

That prospect does not seem to be deterring Japanese firms. Just outside Phnom Penh is a new industrial park set up to lure Japanese manufacturers such as Minibea, which makes tiny motors for mobile phones, and Ajinomoto, which makes food seasonings. There is a constant stream of new tenants; the zone is now in its third phase of development, says Hiroshi Uematsu, who oversees it. “As a private firm, you need to go somewhere,” he says.

No comments:

Post a Comment