June 29, 2016

Friends With Benefits? Russian-Chinese Relations After the Ukraine Crisis

Facing sanctions from the West after the annexation of Crimea, Russia has reoriented its economy toward China. The results of the shift are mixed, but if trends continue, Moscow is likely to drift further into Beijing’s embrace. An asymmetrical interdependence is emerging, with global implications.

Facing sanctions from the West after the annexation of Crimea, Russia has reoriented its economy toward China. In making the pivot, it sought to break its diplomatic isolation, secure a market for its energy resources, and gain greater access to Chinese credit and technology. The results of the shift are mixed, but if trends continue, Moscow is likely to drift further into Beijing’s embrace. An asymmetrical interdependence is emerging, with global implications.

An Increasingly Unbalanced Relationship

Russia’s economic outreach to China predates its annexation of Crimea and the imposition of Western sanctions, but it has intensified following the Ukraine crisis.

In trying to reorient its economy quickly, Moscow has eased informal barriers to Chinese investment.

There was a sharp decline in trade between China and Russia in 2015 and difficulties in negotiating new megadeals. Still, the rapprochement has accelerated projects that have been under discussion for decades, resulting in agreements on a natural gas pipeline and cross-border infrastructure, among other deals.

Chinese financial institutions are reluctant to ignore Western sanctions, but Moscow and Beijing are developing parallel financial infrastructure that will be immune to sanctions.

New deals in the railway and telecommunications sectors may set important precedents for bilateral relations. These projects could reduce Russia’s technological links with the West and increase its dependence on China.

The Russian-Chinese relationship is increasingly unequal, with Russia the needier partner. Without viable alternatives, Moscow may be willing to accept the imbalance.

Lessons for Western Leaders

Russia and China are not entering into an anti-Western alliance. Beijing does not want to confront the West over issues it sees as a low priority, such as Ukraine. Moscow prefers not to be dragged into growing U.S.-China rivalry or territorial disputes in the Asia-Pacific.

Still, Moscow’s growing dependence on China and its tendency to see conflict through an anti-American lens is forcing it to support Beijing in some disputes it would prefer to avoid.

Russia’s military-industrial complex is opening up more to the Chinese market. This shift may affect the strategic balance in Taiwan, the East China Sea, and the South China Sea as the Chinese military gains access to advanced equipment.

Central Asia is a potential arena for rivalry between Moscow and Beijing. Attempts to coordinate the countries’ regional economic integration projects have been unsuccessful. Yet Moscow hopes it can serve as regional security provider while China presides over economic development—a departure from a previous collision course.

Moscow and Beijing are learning from each other’s experience limiting Western influence, providing examples for other authoritarian countries.

Russia Embraces China: Turning Fears Into Hopes

When the crisis in Ukraine erupted in 2014, no one in the Kremlin was expecting a prolonged confrontation. But as soon as sanctions were mentioned for the first time in the West, the Russian government organized a series of brainstorming sessions to analyze how different scenarios might hurt the Russian economy. The conclusion was clear: Russia’s Achilles’ heel was its near-total dependence on Western markets for its hydrocarbon exports, capital, and technology.1 The historical cases of sanctions regimes presented by Russian analysts at these discussions, ranging from North Korea to Iran, suggested that in order to withstand Western pressure a country needed a strong external partner.2 The only obvious candidate that fit the bill was China—the largest economy that did not plan to impose sanctions on Russia.

This was the context in which, in May 2014, the Russian leadership embarked on a new and more ambitious pivot to China. The strategic goal was not only to deepen the political relationship but also to reorient the Russian economy toward the East. It was hoped that China would become a major buyer of Siberian hydrocarbons, Shanghai and Hong Kong would become the new London and New York for Russian companies seeking capital, and Chinese investors would flock to buy Russian assets, providing badly needed cash, upgrading the country’s aging infrastructure, and sharing technology.3 Put simply, the new pivot would keep the Russian economy afloat and spur new sources of growth.

For its part, China neither supported Russia’s actions in Ukraine nor directly criticized them. But it welcomed Moscow’s policy of going East. The rupture between Russia and the West over Ukraine was seen as something that would help China to secure a Russia more accommodating to Beijing’s commercial demands and more willing to give up on ambitions of deep integration with the West—a nightmare scenario for Chinese strategists.

With some exceptions,4 this new apparent rapprochement was greeted with considerable skepticism in the West.5 The dominant view in Western capitals was that relations between Moscow and Beijing would always remain an “axis of convenience.”6 Relations with the West and with the United States in particular, it was argued, are more important for China than its ties to Russia, given that U.S.-Chinese trade volumes were six times greater than Russian-Chinese trade flows in 2014 and ten times greater in 2015. More importantly, Western analysts predicted that deep mistrust between the countries’ elites, historical territorial disputes, an unbalanced structure of trade, the Chinese economic and demographic threat to Siberia and the Far East, competition for influence in Central Asia, and the overall growing inequality between the two countries would preclude any meaningful partnership.

Two years after Moscow began its China pivot, some developments confirm this skeptical view. Western commentaries have often adopted a mocking tone about the exaggerated hopes that Moscow has placed on Beijing. “Mr. Putin may hope that such arrangements [with China] can help shield Russia from western sanctions. Yet, in his heart of hearts, he must know that Beijing is not going to do Moscow any favours,” argued a May 2015 editorial in the Financial Times.7 Thomas S. Eder and Mikko Huotari from the Berlin-based Mercator Institute for China Studies wrote inForeign Affairs that

What one finds time and again with Sino–Russian cooperation are lofty announcements that fail to correspond with the reality of a less than robust relationship. As a result, the current state of Sino–Russian relations do [sic] little to provide Moscow with any geopolitical leverage against Europe. In fact, it is the other way around. Europe has been more successful at playing the diversification game, as well as attracting investments and increasing trade with China.8

Yet, the new Russian-Chinese rapprochement may be more serious than this line of reasoning suggests. In the wake of the Ukraine crisis, the Russian leadership took a fresh look at many issues that had been blocking cooperation with Beijing for years. This process resulted in the removal of three key informal barriers. First, Moscow decided it had been too reticent about selling advanced weaponry to China. Second, Moscow chose to review a de facto ban on Chinese participation in large infrastructure and natural-resource projects. Third, the Kremlin reassessed its relationship with China in Central Asia, which had hitherto been defined as largely competitive with very limited opportunities for collaboration.

The new approach that the Kremlin adopted yielded few successes in 2014 and 2015. But the deals concluded or under discussion may presage more meaningful developments in the future, putting Russia on a path where it ends up accepting the role of a junior partner in an increasingly asymmetrical relationship. Moscow may end up providing crucial resources that Beijing needs (such as military technology, natural resources, and access to new markets) to boost the latter’s ambition to be the next global superpower in exchange for an economic and financial lifeline.

One of the central factors that is propelling the new Russian-Chinese relationship is the personal connection between the two countries’ leaders, Vladimir Putin and Xi Jinping.

Boris Yeltsin’s relationship with his Chinese counterpart, Jiang Zemin, was good. They spoke in Russian, which facilitated direct conversation, but the Russian president never called his Chinese colleague “friend,” as he addressed former U.S. president Bill Clinton and former Japanese prime minister Ryutaro Hashimoto. Putin’s experience with Jiang was fruitful but brief. Both leaders managed to sign the 2001 Friendship Treaty, which paved the way for the settlement of Russian-Chinese border disputes. Jiang’s successor Hu Jintao was ten years older than Putin and unemotional. Various interlocutors describe Hu as wearing the same inscrutable face in all situations.

Xi has been very different from both his predecessors. Just six months younger than Putin, Xi could be described as the Russian president’s soul mate—a strong leader with a vision of his country becoming a great power again. Xi’s remarks in Mexico in 2009 about “some foreigners with full bellies and nothing better to do [than] engage in finger-pointing at us” did not go unnoticed in Moscow.9 Extended profiles of him bear a lot of similarities to what is publicly known about Putin.10 The two men have developed deep personal ties despite the language barrier, according to those who have observed the relationship up close.

The first personal meeting between the two took place in March 2010 in Moscow, when Putin was prime minister and Xi was vice president of the People’s Republic of China (PRC).11 But it was on October 7, 2013, that the relationship became truly personal. The two leaders met on the sidelines of the Asia-Pacific Economic Cooperation (APEC) summit in Bali—it was Putin’s birthday and the last meeting of the day for both leaders. Negotiations turned into a private birthday party with very few people present and many celebratory toasts, which helped cement the bond between them. Given the importance Putin attaches to personal diplomacy, this new level of contact with the Chinese leader was an important factor behind Moscow’s changed approach.

In 2014, following internal deliberations, the Kremlin decided to reach out to China to foster an economic partnership in a more direct fashion than before. Informal political barriers limiting Chinese investment in Russia were eased. At the Krasnoyarsk Economic Forum in February 2015, Deputy Prime Minister Arkady Dvorkovich announced that Chinese companies would now be welcome to buy assets in the natural-resource sector. They also were permitted to bid on infrastructure contracts in sensitive industries like roads and railways, which for a decade had been carefully protected from competition by powerful Russian lobbies. Chinese financial institutions were informally encouraged to expand their presence in the Russian market to fill a gap vacated by Western firms. High-level Russian officials delivered these messages through a series of unannounced visits to Asian financial capitals, while they were exploring opportunities for Russian debt and equity listings.12

Moscow also significantly upgraded its mechanisms for communicating with Beijing. While Washington has maintained various channels of correspondence with Chinese elites and political leaders for many years, Russia’s links had remained primitive. Now in addition to the existing intergovernmental commission for preparing prime ministers’ meetings (co-chaired by Russian Deputy Prime Minister Dmitri Rogozin and Chinese Vice Premier Wang Yang) and an already-established strategic dialogue on energy issues (co-chaired by Deputy Prime Minister Dvorkovich and China’s highest-ranking vice premier, Zhang Gaoli), a new intergovernmental commission was formed. The new commission is co-chaired by Russian First Deputy Prime Minister Igor Shuvalov, Putin’s powerful point man for economic troubleshooting, and Zhang, who is also one of seven members of the Chinese Communist Party’s (CCP) powerful Politburo Standing Committee. Shuvalov’s commission has become the key institution for negotiating large-scale bilateral projects. In addition to these bodies, Putin appointed his longtime friend Gennady Timchenko to chair the Russian-Chinese Business Council.13 Timchenko ranks fifth on the Forbes list of wealthiest Russian citizens,14 and was added to the U.S. Treasury Department sanctions list after the annexation of Crimea. By putting in place a capable bureaucrat and a personal friend with direct access to the Russian leader himself, Putin has moved the bilateral business agenda to a new level.

Aside from these pragmatic business matters, an attempt by the Kremlin to forge emotional bonds with Chinese elites on the basis of a common world outlook constituted a kind of group psychotherapy for the Russian leadership after the trauma of the Ukraine crisis. An uneasy sense of isolation and feelings of rage about what was viewed as betrayal by the West was combined with the sense of belonging to a resurgent great power after the incorporation of Crimea into Russia, and this created a strong need for international soul mates.15 Pressure from the West, it was believed, would bring Russian and Chinese elites much closer together than before. A nation-building narrative centered on pride and the revival of the glorious past has been strong in China since a patriotic education campaign was launched in the 1990s.16 This national story became dominant in China after Xi acceded to power and promoted his ambiguous China Dream concept. A similar narrative became increasingly important in the Russian context, particularly after the takeover of Crimea.17

Both regimes have invested a lot in commemorating historic events, especially the victory in World War II. For modern Russia, the victory in what it calls the Great Patriotic War forms the moral foundation of many Russians’ identity. For the CCP, memories of the war against Japan, its enormous human cost, and the role of the Communists in the national resistance still form one of the pillars of the party’s legitimacy. Attempts to question or downplay the role of either country during World War II are viewed in Moscow and Beijing as attacks on their prestige and on the core ideological foundations of the regimes.18 But this patriotism is more than just cold-blooded calculation: it has deep roots in the genuine personal emotions of the leaders. After all, Xi’s father, Xi Zhongxun (1913–2002), took part in the war against Japan, and Putin’s father, Vladimir Spiridonovich Putin (1911–1999), fought in the war against Germany.

It therefore came as no surprise when Xi Jinping was the guest of honor at the 2015 Victory Day parade in Moscow, an event boycotted by U.S. President Barack Obama and other Western leaders. Putin returned the favor and was the guest of honor during the celebrations in Beijing on September 3, 2015, the first parade in PRC history to commemorate the victory over Japan. The decision of Western leaders to skip both these important events in protest of Russia’s annexation of Crimea and growing Chinese assertiveness in the South China Sea was perceived in Moscow and Beijing as a coordinated plot to deny both countries their rightful place in history.

Throughout 2014 and 2015, attempts were made to bring both societies closer together and to overcome lingering mistrust through the careful use of both government propaganda and state-controlled media. Since 2006, Russian state-run television channels have observed an informal ban on negative coverage of China. There is growing evidence that Xi has authorized the same policy vis-à-vis Russia. The CCP Propaganda Department tells editors at Chinese state-controlled news agencies like Xinhua and television channels like China Central Television (CCTV) to be careful in how they cover Russia in general and to avoid criticizing Putin personally. This stance was evident during the coverage of the Panama Papers scandal, when mainland Chinese media avoided mentioning both Chinese and Russian leaders that were implicated. Search results were also erased from Weibo, China’s most popular microblogging platform.

These efforts have yielded results, at least in Russia. According to polls conducted by the independent Levada Center,19 Russians’ positive attitudes toward China peaked in May 2014, with 77 percent of respondents viewing China positively and only 15 percent seeing it in a negative light (see figure 1). This is a stark contrast not only to the figures of two decades ago (48 percent positive and 21 percent negative, respectively, in March 1995) but also to the figures from just a year before the Ukraine crisis. In November 2013, only 55 percent of respondents viewed China positively and 31 percent saw it negatively.

The speed and intensity of these mood swings demonstrate the considerable influence of mass media and the knock-on impact of average Russians’ anger toward major Western powers as a result of the Ukraine crisis. Some Western commentators cite conventional wisdom that average Russians harbor negative feelings toward China,20 but empirical evidence that supports such assertions is hard to come by. Russian elites’ long-standing cautious attitudes toward China are a separate matter, but this mind-set has undergone significant changes as a direct result of the Ukraine crisis.

China’s Russia Gambit: Any Takers?

Beijing’s pre-2014 Russia policy was made significantly more complicated by the Ukraine crisis. Policy debates in Beijing about the crisis, Russia’s eastward drift, and the dramatic changes in the global strategic environment created by these developments unfolded quickly, as the Chinese leadership watched the sudden departure of Ukraine’s then president Viktor Yanukovych, and then Putin’s bold step of annexing Crimea outright. These events, according to Chinese foreign policy experts advising the country’s top officials in Zhongnanhai, caught China’s leaders off guard just as they did Western leaders. The major challenge for Beijing in the initial stage of the crisis was to carefully navigate a sensitive issue, which involved many of China’s important political and economic partners, even though it did not affect China directly.

The public stance that Beijing took was predictable enough. The Chinese Ministry of Foreign Affairs stuck to its usual mantra about respect for international law and resolving the conflict by peaceful means. Yanukovych’s abrupt departure after demonstrations on the Maidan turned violent alarmed Beijing, stirring up Chinese suspicions about U.S. involvement in support of color revolutions around the world. Russia’s aggressive response to what was viewed as Western intrusion garnered sympathy among some Chinese elites. Early comments by a Chinese Ministry of Foreign Affairs spokesperson, Hong Lei, following the toppling of Yanukovych, reflected this point of view.21

As Moscow later moved to annex Crimea, the situation became decidedly more complicated for Beijing. China has a negative view of the very idea of outside forces supporting separatism on ethnic grounds in light of lingering ethnic tensions in the country’s western regions of Tibet and Xinjiang—not to mention the Taiwan issue. China’s propaganda department issued a warning to domestic media that they “may not connect the . . . [Crimea issue] to our own country’s issues with Taiwan, Tibet, or Xinjiang.”22 Beijing’s stance on Ukraine during this period amounted to careful maneuvering and a concerted effort not to take sides in the conflict. China abstained from voting on a Western-backed UN Security Council resolution that condemned the Crimea referendum, supported Ukraine’s territorial integrity, and called for the non-use of force.23 At the same time, Chinese officials were careful to avoid direct criticism of Russia while consistently condemning the West’s sanctions policy.

Internal discussions on the consequences for China of Russia’s rupture with the West were more intense, according to open-source information and conversations with Chinese officials and experts. The dominant view in the Chinese leadership was that the Ukraine crisis presented both challenges and opportunities. Chinese leaders were surprised by the degree of the Kremlin’s unpredictability. The decision to annex Crimea and to directly challenge the U.S.-led international order—and to pay a huge economic price for doing so—was, in Beijing’s view, irrational and against Russia’s long-term interests. Concerns that Russia was worryingly unpredictable were later confirmed by Moscow’s direct involvement in Syria and the rapid escalation of tensions with Turkey, neither of which Chinese experts anticipated. Another risk was that the tensions between Russia and the West would escalate and put greater pressure on China to take sides.

However, it was the opportunities side of the ledger that was reportedly highlighted during the CCP’s Foreign Affairs Leading Small Group meetings in April 2014. Isolated from the West, Russia was expected to reach out to Beijing and become more eager to open up its economy to Chinese companies. Also, it was hoped that Washington’s preoccupation with the Russia challenge would shift U.S. attention away from its own pivot to Asia and give Beijing additional breathing room. This view was particularly strong in the military, as could be seen from public comments by People’s Liberation Army (PLA) Major-General Wang Haiyun, a former defense attaché in Moscow.24 Influential scholars like Yan Xuetong of Tsinghua University, retired generals like Wang, and even retired senior diplomats publicly called on the Chinese leadership to use the situation to forge a closer quasi-alliance with Moscow.25 Wang, one of the most vocal advocates of a closer partnership, called for the two countries to pool their economic and foreign policy resources and take advantage of their inherent complementarity. “Russia is a master in boxing, while China is skilled in tai chi,” he wrote in a Chinese-language op-ed for the Global Times.26

The top leadership formulated a more cautious position. According to several Chinese interlocutors, before Putin’s visit to Shanghai in May 2014, Xi gave personal instructions to key members of the State Council and the top managers of key state-owned enterprises (SOEs). His main message was that corporate players should actively seek new opportunities in Russia but avoid overtly exploiting Russia’s difficult situation or seeking one-sided deals at knockdown prices. In Beijing’s view, the oversized appetites and aggressiveness of Chinese investors could contribute to undesirable tensions in the future and eventually encourage Russia to make another U-turn in order to mend relations with the West. At the same time, SOEs were told that they should not engage in projects that made no economic sense.

This cautionary advice from Zhongnanhai came just as the largest Chinese SOEs were beginning to feel the aftermath of three simultaneous shocks. China’s ongoing anticorruption campaign—which began as an investigation into Zhou Yongkang, a former member of the Politburo Standing Committee and China’s energy czar—eventually wiped out many of the top managers of leading energy companies. Their replacements needed time to catch up on the details of what had already been discussed with their Russian counterparts. The anticorruption campaign soon eliminated any incentives for proactive initiative on the part of managers and bureaucrats—in times of big purges, passivity is obviously the safest strategy. New, stricter requirements for SOE efficiency, established at the CCP Central Committee’s Third Plenum meeting in November 2013, presented an additional obstacle to greater involvement in Russia. The slowdown of the Chinese economy further complicated matters. The scale of China’s economic challenges was not widely apparent during the initial stage of Russia’s pivot to Asia in mid-2014. Yet within a few months, the slackening demand for natural resources and sharp price declines in major global commodities markets pulled the rug out from under potential projects, including in the energy sector, which historically has been the most crucial sphere for bilateral economic cooperation.27

Fueling the Dragon

Energy forms the backbone of Russian-Chinese trade, but attempts to radically increase the volume of energy trade between the two countries over the past two years have had mixed results. Energy exports, of course, are of vital importance for sustaining Putin’s regime and Russia’s overall economic prospects. Direct and indirect earnings from hydrocarbons account for upward of 70 percent of Russia’s budget revenue, according to some estimates.28 China became a net importer of oil in 1994, and the country has worked assiduously to secure access to new energy sources to power its economic growth, preferring to do so through land-based pipelines.29 Prior to the economic slowdown, access to Russian natural gas became increasingly important amid projections of increased Chinese domestic demand, attempts to reduce dependence on coal, and mounting political concerns about pollution in big cities as well as other ill effects of China’s rapid modernization.

Gas

In the gas sector, there are tentative signs of progress, but the situation is still far from rosy. The two sides managed to sign a long-awaited gas deal during Putin’s visit to Shanghai in May 2014. The gas will be delivered from two as-yet undeveloped fields in Eastern Siberia, Kovykta and Chayanda, via the new Power of Siberia (or Sila Sibiri) pipeline, which will pump 38 billion cubic meters of gas annually until 2030. While the parties did not disclose the price at which Russia will be selling this gas, the reported total value of the contract was $400 billion. At the time the deal was signed, the price of oil was over $109 per barrel. Today the price for the Brent crude oil benchmark is less than half that, which matters greatly given the use of oil-index pricing in the contract. Alexey Miller, the chief executive officer (CEO) of the major Russian natural-gas firm Gazprom, expressed his pleasure with the deal, declaring at the September 2014 Sochi International Investment Forum that in just one day “our esteemed Chinese partners came near Germany, our major gas consumer.”30

Two years later, this project is facing major challenges. The Chinese side has refused to provide a planned $25 billion loan needed for pipeline construction, and Russian officials have complained that the conditions on offer from Beijing—requiring the participation of Chinese companies in the construction phase—are unacceptable.31Several Gazprom tenders for the pipeline were canceled in 2015 at the request of Russia’s Federal Antimonopoly Service.32 More importantly, those familiar with Gazprom’s financing models for the Power of Siberia pipeline say that the project may remain unprofitable if the oil price does not increase significantly in the next fifteen years;33 the pipeline could be used for another contract after 2030, allowing Gazprom to actually turn a profit. The Soviet Union followed the same logic in 1970 when it signed a gas-for-pipes agreement with West Germany. The first contract was used to finance the construction of expensive infrastructure, which allowed the Soviet Union to earn hard currency later on, after the construction costs had been fully paid off.34

All the same, officials on both sides remain confident that the pipeline will be built, though perhaps with delays. Construction has begun on both Russian and Chinese territory.35 The fact that the main contractors on the Russian side include companies owned by Gennady Timchenko (Stroytransgaz) and Arkady Rotenberg (Stroygazmontazh), members of Putin’s inner circle, has further boosted confidence in the project.36 After Gazprom abandoned its massive South Stream and Turkish Stream projects in Europe, freed-up cash flows could be diverted to the Power of Siberia pipeline, which will receive active government support in the form of tax exemptions and other incentives. However, while some Chinese sources are certain that the pipeline will eventually be commissioned, there is still no clarity on the matter of the Chinese loan. If credit is needed and China continues to demand the involvement of its construction companies, it is possible that Rotenberg’s and Timchenko’s firms may ultimately be forced to form consortiums with Chinese companies.37

For now, prospects for other Gazprom projects targeted at the Chinese market remain bleak. Moscow offered to build a pipeline across the Altai Mountains to Xinjiang (the so-called Western Route or the Power of Siberia II pipeline), which would have a capacity of 30 billion cubic meters of gas per year. Unlike the first Power of Siberia, this pipeline could be built on existing infrastructure, requiring less construction work, and would allow Gazprom to pump gas to China from existing fields in Western Siberia. Moscow seeks to pit its Western and Eastern customers against each other while supplying gas from the same fields to both sides. Following years of negotiations, a detailed framework agreement was signed during Xi’s May 2015 visit to Moscow,38 but a commercial contract between Gazprom and the China National Petroleum Corporation (CNPC) setting a price for the project’s gas does not appear to be imminent.

The main reason for the delay is a disagreement over the price: Russia and China are using different benchmarks. Gazprom is basing its desired price on its existing contracts with Germany or possibly the Power of Siberia price it settled on with China. But for the CNPC, the preferred benchmark is far cheaper Turkmen gas pumped into Xinjiang through a pipeline commissioned in 2010. Russian gas would require expensive infrastructure to carry it from an entry point in Xinjiang to major consumption hubs in China’s eastern provinces. Given the abundance of imported liquefied natural gas (LNG) and the scaling-back of projected demand for imported gas due to the economic slowdown and more efficient coal use by a new generation of Chinese power plants, the western route now appears to be a nonstarter, as do Gazprom’s plans to build a third pipeline for Sakhalin gas to China via Vladivostok. Although the company signed a memorandum of understanding with the CNPC, and an 8-billion-cubic-meter pipeline between Sakhalin and Vladivostok, which was built before the 2012 APEC summit, is already operational, there are lingering problems with the resource base.39

Oil

The Russian sector that made the most significant gains in the Chinese market in 2014 and 2015 was oil, despite the collapse in prices. The foundations for a partnership were established in 2005, when Russia’s state-owned Rosneft began supplying oil to China via railway to service crucial Chinese loans, which had enabled the firm to buy Yuganskneftegaz, a key part of another Russian oil company, Yukos, which was nationalized following the jailing of fallen oligarch Mikhail Khodorkovsky. (Western banks had refused to provide loans to cover the transaction amid fears that Yukos’s shareholders would use the courts to press their claim to their former assets.)

The 2009 pipeline deal paved the way for a massive increase in Russian oil exports to China, despite price disputes between Rosneft and the CNPC, which resulted in a $3 billion loss in revenue for the Russian company. Moreover, in 2013, Igor Sechin, the powerful chair of Rosneft and a close ally of President Putin, agreed to accept $60 billion in loans from Chinese companies as part of what was termed a prepayment scheme backed by future oil deliveries. The money was then used for Rosneft’s domestic expansion, including its landmark purchase of Russia’s third largest producer, TNK-BP, in 2013. Now, with oil prices 50 percent below 2013 levels, Rosneft is struggling financially to contend with these challenging new realities even as it fulfills its obligations and delivers the promised oil to the Chinese. In addition to increasing the capacity of the Skovorodino-Mohe pipeline, Rosneft has begun selling oil out of the Kozmino port on the Pacific Coast—with 60 percent of it now going to China40—as well as through Kazakhstan,41 which has increased Russia’s share of Chinese oil imports (see figures 2 and 3). At various points in 2015 and 2016, Russia actually surpassed Saudi Arabia as China’s lead supplier.42

Increased deliveries notwithstanding, the Russian oil industry was dealt a huge blow when oil prices plummeted in 2015. The collapse was immediately reflected in the overall trade volume between China and Russia—just as the surge in global oil prices in the 2000s played a significant role in a rapid trade expansion. Between 2003 and 2012, trade between the two countries grew at an average of 26.4 percent per year. In 2011, then presidents Dmitry Medvedev and Hu Jintao announced their goals of achieving $100 billion in bilateral trade by 2015 and $200 billion by 2020. Initially, these targets seemed attainable. In 2014, trade grew by 6.8 percent, reaching a total of $95.3 billion, but in 2015 it collapsed by 28.6 percent, totaling just $68 billion. Russia dropped from being China’s ninth-largest trade partner in 2014 to sixteenth place in 2015. The decline was not attributed solely to the drop in commodity prices; the drop in trade with China’s other commodity suppliers, such as Australia and Brazil, was not nearly as steep.43 The key factor appears to have been the economic decline in Russia that same year, as GDP decreased by 3.4 percent, and the subsequent low purchasing power of Russian companies and households—seen in the sharp drop in Russian imports from China. The only silver lining for Russia was the effective disappearance of an imbalance between its exports to and imports from China (see figure 4).

The plunge in oil prices in 2015 also created new obstacles for cooperation on investment projects. Rosneft offered the CNPC a 10 percent stake in its flagship oil field, Vankor, the major resource base for the Eastern Siberia–Pacific Ocean (ESPO) pipeline. In November 2014, the Russian Minister of Energy Alexander Novak suggested that Rosneft might accept payment for the stake in Chinese renminbi.44Meanwhile, Putin told the TASS news agency that Russia was ready to switch trade in Vankor oil from U.S. dollars to national currencies.45 However, the Russians appeared to have unrealistic expectations about the potential price for the minority stake in Vankor, and the Chinese eventually suspended negotiations. The Oil and Natural Gas Corporation Limited, an Indian company, is as of mid-2016 in the process of acquiring the stake in Vankor, provoking additional dissatisfaction from Beijing. Chinese investors have also expressed interest in stakes in other Russian oil companies, according to Russian Finance Minister Anton Siluanov.46 There have been unconfirmed suggestions in Chinese analytical circles that Russia might ultimately sell a large stake in Rosneft to a Chinese oil company or financial institution for a symbolic price, and that such a purchase might provide Rosneft with a helpful write-down of its debt under the prepayment agreement and other loan arrangements. The Russian government currently is discussing the sale of a 19.7 percent stake in Rosneft to various foreign investors, including the possibility that the CNPC may purchase 7 percent of it. According to CNPC First Vice President Wang Zhongcai, the company is actively looking into the deal and has formed a study group to explore the opportunity.47

Though the practices are still in their infancy, the use of Chinese technology in offshore drilling and renminbi-denominated oil contracts represent two important recent developments in the oil sector. The first experiment in this area was Rosneft’s September 2015 contract with China Oilfield Services Limited, a subsidiary of the China National Offshore Oil Company, involving the drilling of two oil wells in the Sea of Okhotsk.48 At the drilling site, the sea has a depth of only 150 meters (around 500 feet), which means it does not qualify as deep-sea drilling under the provisions of U.S.- and EU-led sanctions. As many international oil-service companies have become cautious about Russian projects in the areas covered by sanctions, the introduction of advanced Chinese technologies could increase Russian oil companies’ reliance on China in the oil-service sector, which is already dominated by Chinese producers in some subsectors such as drilling platforms. The dependence on China, however, is expected to remain limited, given that the Russian oil-service industry is dominated by local champions like Eurasia Drilling and the subsidiaries of major international energy firms. For the time being, Chinese service companies clearly cannot match the technologies or capabilities of major global oil companies or leading oil-service firms such as Halliburton and Schlumberger.

The second, more promising, experiment was launched by Gazprom-Neft, Gazprom’s oil subsidiary, which announced that it will sell oil from the ESPO pipeline to Chinese customers for renminbi.49 Despite the hyped claim that this transaction will undermine the global dominance of dollar-based transactions, the pricing of oil is still tied to the dollar-denominated Brent benchmark. According to interviews with managers of Russian oil companies, the logic behind this move is that the use of renminbi to purchase Chinese equipment will prevent conversion losses and hedge against currency risks, thus saving Russians about 5 to 7 percent of the contract price, as well as move payments out of the orbit of the U.S. banking system. If this scheme becomes widespread, it could help immunize the Russian-Chinese oil trade against risks associated with possible future Western sanctions.

Any Market for a Bear?

A central goal of Moscow’s pivot to China was greater access to Chinese credit. Hopes that this objective would be obtained were fueled by Beijing’s critical stance toward the U.S.- and EU-led sanctions regime. Chinese Vice Premier Zhang Gaoli told President Putin on September 1, 2014, that he “want[ed] to make it clear that China categorically opposes the sanctions the United States and Western countries have taken against Russia.”50 However, Russian companies quickly discovered that Chinese financial institutions could be as strict as or even stricter than some Western banks about compliance with the sanctions regime.

Public complaints about Chinese partners’ “ambiguous position regarding Russian banks in the wake of US and EU sanctions,” as Russian banker Yuri Soloviev put it, began to be voiced in the summer of 2015, a year after Putin’s triumphant visit to Shanghai.51 Soloviev, the first deputy president and chairman of the second-largest bank in Russia—state-owned JSC VTB Bank—used the following words, in a June 16, 2015, op-ed in Finance Asia: “Most Chinese banks will currently not execute interbank transactions with their Russian peers. In addition, Chinese banks have significantly curtailed their involvement in interbank foreign trade deals, such as providing trade finance.”52 Later, in September 2015, Soloviev’s colleague Vasily Titov complained that Chinese banks were “too rigorous” in observing Western sanctions and that it took two weeks to clear payments through Chinese banks when it had taken just three days before the sanctions were introduced.53

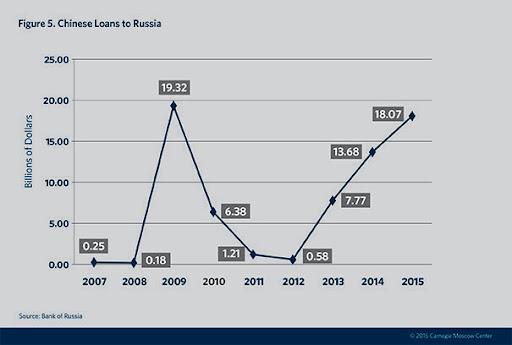

Publicly available data indicate that sanctions have indeed had a negative effect. In 2014 and 2015, no Russian companies managed to issue debt or equity on Chinese stock exchanges including Hong Kong. Local regulators and financial institutions appear to harbor bad memories of Rusal’s ill-starred initial public offering. In addition, this negative sentiment was reportedly strengthened by friendly words of caution from U.S. Treasury and State Department officials.54 Russian investors were also wary of Shanghai after the equity rout that began in the summer of 2015. Credit lines amounting to 9 billion renminbi that Russia’s Sberbank, the JSC VTB Bank, and Chinese lenders signed in May are barely being used because there is no demand in Russia for loans in renminbi, according to Maxim Poletaev, the first deputy chairman of Sberbank’s executive board.55 At the same time, Chinese banks have been reluctant to provide loans in much-needed U.S. dollars or euros. In rare cases when Chinese credit has been extended to Russian companies, these transactions have largely been syndicated loans involving China’s four largest banks working in coordination with other international players. This funding is offered only to well-regarded corporate borrowers like Novolipetsk Steel,56 which are not under sanctions and continue to enjoy access to Western credit.57 Other rare success stories include the $2 billion credit line that the London subsidiary of the Bank of China provided to Gazprom.58 This deal appears to be a goodwill gesture connected to the Power of Siberia pipeline construction ahead of Putin’s visit to China in June 2016. Data from the Central Bank of Russia show that the number of loans originating from China rose throughout 2014 and 2015 from a very low baseline, but the total amount is small and can in no way replace previous flows of credit from Western financial institutions (see figure 5).59

Broadly speaking, there are three main reasons for Chinese bankers’ reticence about the Russian market.

First, there is no overlooking the fact that Western markets are far more developed and attractive to Chinese banks even when those banks are presented with favorable terms to tap into the Russian market more deeply. In 2015, China’s trade in goods with the United States was $598 billion,60 while Chinese trade with Europe in goods for the same year totaled 520.9 billion euros (about $583.4 billion).61 Chinese state-owned banks were also recently allowed to buy stakes in U.S. and European banks after years of suspicion and long-standing bans. In Russia, China’s four largest banks have never been allowed to buy local players, and the former’s expansion into the retail sector was subject to additional levels of scrutiny—at a time when investment by French, British, and Italian competitors was encouraged. Moreover, Beijing has recently embarked on a quest to promote the renminbi as a global currency, and China’s four major banks are trying to carve out significant roles in terms of clearing payments and making markets in Europe and the United States. The choice between jeopardizing relations with the regulators of large, profitable prospective markets and entering the relatively tiny, risky, and overregulated Russian market was an easy one for major Chinese financial players.

Second, China’s banking sector lacks expertise on Russia. While Chinese banks have capable teams on the ground in Moscow and the Far East, these are no match for the pool of Russia experts that European and U.S. banks have at their disposal. As risk compliance grows increasingly synonymous with navigating the U.S. and EU sanctions regime and circumventing what could be termed toxic gray areas, the cost of operating in Russia is prohibitive for many Chinese banks. The first banks to cut back on business with Russia were smaller ones such as Ping An Bank, the Bank of Communications, and China Merchants Bank, which were servicing the accounts of companies from offshore jurisdictions used to clear payments with Russia. The banks have asked some customers to close their accounts because they “were engaged in some activities with Russia,” according to a Rosbalt news report.62Russian and Chinese banking representatives indicate privately that the same situation has taken hold in Hong Kong, where local banks have become extremely reticent about opening bank accounts for Russian as well as Ukrainian citizens.

Last but not least, the political environment in which state-owned banks are now operating in the wake of the anticorruption campaign does not encourage taking additional risks in Russia.

With the lion’s share of Chinese commercial banks maintaining a cautious stance toward Russia, the only two Chinese financial institutions that have been aggressively signing agreements with Russian partners are the two political banks—the China Development Bank (CDB) and the Export-Import Bank of China (or China Exim Bank).63 These banks—which serve as the political pockets of the Chinese government, so to speak—are less connected to the international financial system, and thus can take greater risks in terms of their exposure to the Russian market.64 Both banks have been active in Russian deals that range from building steel plants to providing credit lines for Russia’s sanctioned state-owned banks.65The most recent example of their involvement in the Russian economy was the late-April 2016 announcement that the CDB and the China Exim Bank will provide much-needed loans for the Yamal LNG project totaling $12 billion over fifteen years, which means that the project has locked in all the external financing it needs ($27 billion in total). The deal is a landmark not only because Yamal LNG is a key part of Russia’s broader strategy in the Arctic and a flagship LNG project but also because Novatek (along with major shareholder Gennady Timchenko) is a target of U.S. and EU sanctions. Total, a French natural-gas producer and a Yamal shareholder, has tried to secure European and Japanese financing for the project, according to Total CEO Patrick Pouyanné’s interviews with Kommersant and Asia Nikkei, but these efforts failed.66 The same logic applied to a March 15, 2016, deal in which a 9.9 percent stake in Yamal LNG was sold to the Silk Road Fund (SRF) for nearly $1.1 billion—the SRF is a $40 billion investment fund that China established in 2014 to support President Xi’s Silk Road Economic Belt initiative.67

Amid sluggish demand and depressed global gas prices, many international majors are delaying or shelving big-ticket LNG projects, which makes the timing of the Chinese interest in the Yamal project particularly curious.68 According to Chinese interlocutors, both deals were personally blessed by Xi and intended as a gesture of goodwill to the Kremlin, given Timchenko’s role as a member of Putin’s inner circle and his point person for China. While the personal involvement of the two countries’ leaders helps explain the impetus behind the Yamal LNG deal, it also seems likely that the selective use of financial institutions with limited exposure to international markets will become the preferred method for future bilateral ventures. There are already calls by Russian experts to establish a “specialized joint Russian-Chinese financial unit … which should be immune to any pressure from the United States or the EU,” as Vasily Kashin put it.69

Another important direction for Russian-Chinese cooperation is the creation of new mechanisms for raising debt in national currencies. In July 2015, before the start of the BRICS summit in Ufa, Chinese investors bought $1 billion in Russian government bonds.70 According to Russian Deputy Finance Minister Alexey Moiseev, both countries’ Ministries of Finance, along with the Central Bank of Russia and the People’s Bank of China, are working on mechanisms that will allow Russia to issue renminbi-denominated government bonds in Moscow targeting mainland-based Chinese investors.71 If successful, this initiative will create a framework for the possible future issuance of so-called panda bonds by Russian corporate players. The first potential issuance may be underwritten by the Industrial and Commercial Bank of China, the Bank of China, and Gazprombank.72 Such efforts are not directly prohibited by U.S. and EU sanctions. Finally, Beijing is urging Russia to join its China International Payment System, an alternative to the Society for Worldwide Interbank Financial Telecommunication (SWIFT).73 These moves will help to lay the groundwork for bilateral transactions that are centered around the renminbi and less tied to international markets, including the U.S. banking system.

Other pieces of the puzzle include an agreement between the Chinese UnionPay credit card system and the Russian Mir payment system due to take effect in 2017, and a pact to recognize each other’s auditing standards and credit ratings. This collaboration between UnionPay and Mir and the auditing and ratings moves reflect Moscow’s desire to break the domination that MasterCard, Visa, and international ratings agencies enjoy over its payments system. Many Russian banks have rushed to get Chinese local ratings issued by Dagong Global Credit Rating, which rather curiously rated Russia’s sovereign debt as less risky than U.S. notes.74

Last but not least, in order to provide liquidity, both countries want to boost access to each other’s currencies. The three-year currency-swap agreement for 150 billion renminbi (about $24.5 billion) announced in October 2014 during Chinese Premier Li Keqiang’s visit to Moscow was not activated due to ruble and renminbi volatility. The instability of the two currencies can be explained by low trade volumes and the small share of bilateral trade cleared through national currencies. According to a May 2015 statement by President Putin, such transactions accounted for only 7 percent of bilateral trade volume in 2014.75

On balance, Russian elites’ hopes that Chinese financing would make up for the loss of Western capital markets appear exaggerated. The last two years have shown that even Chinese state-owned banks are reluctant to run afoul of U.S. and EU sanctions, for fear of jeopardizing their relations with the regulators of their most significant international markets. Still, Russia and China have found ways to finance high-priority deals through special channels, and have embarked on an attempt to create the rudiments of a bilateral financial infrastructure that will be immune to international pressure. China will be playing the dominant role in these arrangements, which could help cement its place as the financial center of gravity across Eurasia.

Technological Links

The Russian-Chinese relationship is also experiencing major shifts in cooperation on infrastructure and technology. Previously, Chinese companies were informally banned from bidding on large infrastructure projects in Russia, most likely due to the Kremlin’s desire to protect local companies from competition—including those with which it had strong ties—as well as Russian fears of an influx of Chinese migrant workers. In May 2015, a consortium composed of a China Railway Group subsidiary called the China Railway Eryuan Engineering Group, the National Transportation Engineering Design Institute of Moscow, and Nizhny Novgorod Metro Design AG was the only bidder for a $400 million contract to design a high-speed rail line between Moscow and Kazan.76 On April 29, 2016, Russian railways reported that China was ready to provide up to $6 billion in loans and that a concession agreement would be signed by the end of the year.77 The Chinese side has also agreed not to seek formal Russian government loan guarantees, reportedly at the direct instruction of President Xi, according to several Chinese interlocutors.78 Previous experience suggests that the project could encounter significant delays, as the Chinese partners are demanding that the lion’s share of equipment be produced in China. Yet the tone of the conversation marks an important shift in Russia’s attitude toward Chinese participation in the development of its infrastructure.

One area of bilateral technological cooperation that is booming is information technology (IT) and hardware. Russian companies had discovered the advantages of working with Chinese telecommunications giants like ZTE and Huawei as opposed to their Western rivals long before the Ukraine crisis. Discussions about the possibility of shifting the procurement of Russian IT network assets used by government bodies from U.S.-produced to Chinese-produced equipment intensified in 2013 after Edward Snowden’s disclosures about surveillance under U.S. National Security Agency programs. In May 2014, Russia’s Ministry of Telecom and Mass Communications established a task force to study whether such a shift was feasible, and by the end of 2015 the process of transitioning to Chinese equipment was well under way. In October 2014, the Voskhod Research Institute—which is administered directly by Russia’s Ministry of Telecom and Mass Communications and provides hardware and IT solutions to state institutions, including many critical systems such as the vote-counting platform used in national and local elections—agreed to buy servers from Inspur, a Chinese company.79 Many financial institutions, including Western-sanctioned banks such as Sberbank and JSC VTB Bank, state agencies, and state-owned companies have started expensive modernization programs to replace U.S.-made equipment.80

Other deals are small in monetary terms but large in their symbolic significance, such as the Jiangsu Hengtong Power Cable Company Limited’s agreement to supply high-voltage cable for the an energy bridge that is intended to supply electricity to Crimea.81 (Western firms are prevented from participating due to the U.S. and EU sanctions program against Crimea.) Faced with overcapacity and fierce competition at home, many Chinese firms are directing their efforts toward overseas expansion and are willing to provide significant discounts in order to secure the first-mover advantage in new markets. From passenger vehicles to complex IT systems, Russia’s process of transferring its technological partnerships from the West to China has already begun in earnest.

Comrades in Arms

The biggest tectonic shift caused by the Ukraine crisis is happening in the most sensitive area of technological cooperation between Russia and China—the military sector. For ten years, Russia had an informal ban on selling its most advanced technology to China. Moscow’s concerns were both military—it feared that weapons sold might one day be used against Russia—and also commercial. The Chinese had a reputation within the Russian military-industrial complex for copying Russian equipment, producing their own versions, and then competing with Russian arms manufacturers in what could be called their natural markets like Myanmar and Egypt.

After the Ukraine crisis, the Kremlin took a fresh look at its old policy and the possible implications of expanding bilateral arms trade with China to include the most sophisticated systems. There were two lines of reasoning in support of relaxing the restrictions. First, Russian analysis of China’s military industry indicated that the sector was far more advanced than previously believed, leading Russian defense officials to worry less about the risk that technology transfer would provide a boost to Chinese competitors in the global arms market. In addition, Moscow learned that many of the systems that the Chinese had allegedly stolen were actually developed by Russian engineers in the 1990s through contracts with Chinese military SOEs. Military technology transfer was poorly regulated and lacked proper supervision at that time, and Beijing, like many others, was simply taking advantage of the chaotic environment. In fact, these contracts helped many Russian military enterprises and engineering teams to survive the severe disruptions of the 1990s.82

The second argument revolved around China’s actual demographic and economic footprint in Siberia and the Far East. Realistic official figures, along with independent studies, have shown that Chinese migration is marginal: at any given moment, there are no more than 300,000 Chinese in Siberia and the Far East, including tourists, exchange students, and legal temporary workers. Illegal migration was curtailed toward the end of the 2000s, and under current economic conditions people in Chinese border provinces prefer to migrate to the rich coastal regions of their motherland, not to Russia’s Far East. This trend has accelerated since the ruble devaluation, as many Chinese businesspeople in Russia, who were previously sending money back home, reportedly are leaving the country and are going back to the PRC.83

These factors have allowed Moscow to reverse its long-standing policy and resume sales of advanced weaponry to China. One of the most important deals so far is the sale of the S-400 Triumph air defense missile complex, which NATO calls the SA-21 Growler. The deal, signed in September 2014, was announced by Anatoly Isaykin—the CEO of Rosoboronexport, the Russian arms-export monopoly—in an April 2015 interview with Kommersant. “If we work in China’s interests, that means we also work in our interests,” Isaykin said.84 China will start receiving the first of four to six consignments of S-400s no earlier than 2018,85 and the price of the contract could reach $3 billion.86 As Vasily Kashin, a Russian expert on military ties with China, wrote in a Carnegie.ru commentary, “it would be naïve to suppose that the Chinese can copy the S-400 systems within a short period; such a task would require many years of effort. Meanwhile, Almaz-Antey, the Russian producer of air defense systems, is already well on its way to developing the next-generation system (the S-500).”87 Thus, the deal makes a lot of commercial sense.

The military and political consequences of the deal are much more important as they increase the PLA’s capabilities. The S-400 has a greater range for identifying targets and a greater maximum firing range (up to 400 kilometers or around 250 miles) than previous-generation systems like the S-300. This will bring significant changes to the military balance in the skies over Taiwan and the Diaoyu (Senkaku) Islands. The PLA now will be better-positioned to control airspace above these regions from mainland positions in Fujian and Shandong Provinces. For Japan, the task of defending the islands will become much more difficult. For Taiwan, the S-400 may be a game changer, since the PLA would be able to shoot down Taiwanese fighter planes as soon as they take off. China could also use the new system to establish an air defense identification zone over the contested waters of the South China Sea. Negotiations on the sale of the S-400 to China started several years ago, but were significantly accelerated by the Ukraine crisis. Russia’s confrontation with the West and its reassessment of the strategic context of Russian-Chinese relations pushed the Kremlin to give its final blessing to the deal.

Another landmark transaction influenced by the Ukraine crisis was China’s purchase of 24 Su-35 fighter jets, which NATO calls the Flanker E; this $2 billion deal was signed in late 2015.88 It is notable that Beijing was the first foreign customer for this advanced system. According to Vasily Kashin’s commentary on Carnegie.ru, purchasing the Su-35s will allow the Chinese Air Force to gauge its success in developing the indigenous J-11 fighter jet and become familiar with Russian solutions to technical problems.89 The Su-35s, which are expected to be delivered beginning at the end of 2016, will also have military significance, reinforcing Chinese dominance in skies over Taiwan as well as strengthening their combat positions in other potential hotspots.

Russian officials and experts differ as to whether Moscow and Beijing should go ahead with more S-400 or Su-35 deals. But Russia’s reenergized military cooperation with China is not limited to these two systems. There are reports that Moscow may authorize sales of its newly developed Lada-class submarine to China.90 Reverse sales are also taking place. For example, after Germany declined to sell Russia diesel engines for its new Project 21631 Buyan-M corvettes due to sanctions, Moscow turned to Beijing to purchase Chinese engines. Another area of increased cooperation is the purchase of Chinese electronic components for Russia’s space program.91 None of these deals would have been possible without the rupture in Russia’s relations with the West, and all of them will have far-ranging consequences for the military balance in the Asia-Pacific.

Regional Cooperation: Toward a Greater Eurasia?

Moscow’s and Beijing’s approaches to regional cooperation in Central Asia are also undergoing a profound change. In the decades since the collapse of the Soviet Union, Russia has viewed the five Central Asian states as belonging to its self-proclaimed exclusive sphere of influence. According to official Russian thinking, Central Asia is an area where Russia not only has centuries-long ties, but also pressing security and economic interests. The Kremlin has viewed the rapid increase in China’s economic and political penetration of the resource-rich region, usually at Russia’s expense, with great unease. Beijing has been at pains to stress its respect for Moscow’s exclusive interests in Central Asia, but clearly perceives a need to secure firm ties with the countries bordering the unstable Xinjiang region and a strong incentive to get access to the region’s vast energy resources.

Xi first unveiled China’s Silk Road Economic Belt project on a 2013 trip to Kazakhstan, and it was later complemented by a maritime component, leading to its being renamed the One Belt One Road (OBOR) initiative. OBOR represents Beijing’s first multidimensional attempt to transform countries around China using a combination of targeted financial and investment incentives, soft power, and military tools. In private conversations, Chinese officials acknowledge that they had major concerns about Russia’s reaction to the unveiling of OBOR, as the Kremlin was initially reluctant to negotiate ground rules for the co-existence of Xi’s initiative and Putin’s pet project, the Eurasian Economic Union (EEU). Beijing’s fear was that Moscow, anxious about its own status as the leading yet greatly diminished regional power, would regard OBOR as an intrusion into Russia’s sphere of influence and therefore pressure the states of Central Asia not to take part in the Chinese project. Chinese leaders were therefore both surprised and relieved when First Deputy Prime Minister Shuvalov first announced at the Boao Forum in March 2015 that the EEU members were ready to cooperate with OBOR. Shuvalov then personally embarked on negotiating a framework document with Beijing on Putin’s behalf.

For the Russian leadership, this was the result of painful internal discussions, in which the economic team led by Shuvalov—with support from Russian experts and members of the business community—sought to win Putin’s support and overcome the concerns of the security establishment. In the end, the Kremlin concluded that the benefits of coordinating the EEU with the Chinese initiative outweighed the risks. It is now understood that China will inevitably become the major investor in Central Asia and the major market for its vast natural resources, due to the complementary nature of the Chinese and regional economies.

According to Russian officials, Moscow and Beijing will strive to achieve a stable division of labor in Central Asia. China, with its deep pockets and hunger for resources, will be the major driver of economic development in the region through OBOR and other projects, while Moscow will remain the dominant hard-security provider through its Collective Security Treaty Organization (CSTO), while also cementing the EEU’s role as a source of norms for the implementation of Chinese investment projects. The Kremlin hopes this formula will satisfy both Beijing—which is still uncomfortable deploying troops outside its borders—and the Central Asian states, which are anxious about a rising China and more accustomed to Russia’s long-standing military presence in the region.

On May 8, 2015, Putin and Xi signed a joint declaration “on cooperation in coordinating the development of the EEU and the Silk Road Economic Belt.”92Moscow and Beijing declared their desire to coordinate the two projects in order to build a common economic space in Eurasia featuring a free trade agreement between EEU members and China. Although the language is still somewhat ambiguous, the document marked a major departure from the Kremlin’s previous course of competition and suspicion. Beijing formally recognized the EEU as a potential negotiating partner on the free trade zone and on rules for the implementation of transnational infrastructure projects. The Eurasian Economic Commission, the supranational body of the EEU, received a mandate from its member states to start negotiations on a trade and investment agreement with China. This issue, which is a stumbling block for both Russia and the Central Asian states given their high levels of protectionism, was declared a distant goal and effectively relegated to an undetermined point in the future.

Of course, the reality has proven to be more complicated than these ambitious hopes. By signing the declaration bilaterally with China, Moscow offended its EEU partners, most notably Kazakhstan. Thus, Astana and other capitals continue to have good reason to reach out to Beijing directly in order to seek investment, bypassing both the EEU bureaucracy and the Kremlin. China also stayed true to its old habit of doing business with Central Asian leaders on a purely bilateral basis, without involving Moscow. During his September 2015 visit to Beijing, Kazakh President Nursultan Nazarbaev signed a declaration of coordination between OBOR and Kazakhstan’s national infrastructure development program, Nurly Zhol. Kazakhstan was the first Central Asian state to actively pitch its investment projects to China, which caused tensions with Moscow. In October 2015, EEU leaders agreed to coordinate their bilateral arrangements with China under the union’s umbrella, but so far not much has happened. It was only in March 2016 at the Boao Forum that Russian Deputy Prime Minister Dvorkovich promised Chinese Premier Li that Russia would provide a list of EEU proposals for investment projects that could help to link up the two initiatives. The first anniversary of the ostensibly historic declaration was thus celebrated quietly in Beijing and Moscow with a silent consensus that the first year of the agreement had basically been a failure. The May 31 EEU summit in Astana also brought no major news regarding EEU-OBOR coordination.

Despite mutual dissatisfaction over the lack of progress on these coordination efforts, the overlapping interests of the two great powers may outweigh their differences. Both Russia and China share a vision of a region run by secular authoritarian leaders with no major interstate conflicts and no outside involvement, particularly of the United States and its allies. Given the extent of U.S. disengagement from the region as the drawdown from Afghanistan continues, and Russia’s relative decline as an economic center of gravity, over the long run Moscow and Beijing may find ways to accommodate their mutual interests outside the framework of EEU-OBOR cooperation, especially as the future of both projects looks dim.

However, rivalry between Russia and China in Central Asia is quite possible and could even accelerate when the long-expected leadership transitions in Kazakhstan and Uzbekistan, the two most important countries in the region, finally take place. Moscow and Beijing lack coordination mechanisms or intensive diplomatic dialogue on Central Asia. Any abrupt departure of leaders in Astana or Tashkent could conceivably trigger a succession crisis. Rival factions of local elites may end up reaching out to Moscow and Beijing for support. While such dynamics are unpredictable, it is not hard to conceive of destabilizing scenarios, which could spur a major rupture between the two powers.

In a similar vein, tensions between Moscow and Beijing in Central Asia may arise if the latter contests Russia’s self-proclaimed role as the lead security provider to the region. So far China officially has avoided steps that might undercut Russia’s position as the preeminent regional military superpower, a status that Russia enjoys thanks to its role in Central Asia through CSTO and its military presence in Tajikistan and Kyrgyzstan. The main venue for Beijing’s participation in regional security arrangements for the previous decade has been the Shanghai Cooperation Organization, which has provided a platform for joint Russian-Chinese military drills. However, China’s growing trade and investment presence in Central Asia is starting to trigger an evolution in Beijing’s long-standing position. The region’s mineral resources are likely to play an increasingly important role in the PRC’s overall energy security. Likewise, risks of instability are growing due to the deteriorating security situation in neighboring Afghanistan and the potential rise of Islamic extremism. As of this writing, the circumstances behind the deadly June 2016 attacks in the Kazakh city of Aktobe remain far from clear, but may provide another indication that even the most stable countries in Central Asia face this threat. Taken together, the Chinese leadership will probably start to think about how to protect its regional economic interests. OBOR-related infrastructure projects and investments may provide yet another reason for China to think about assuming a more active role in providing regional security and physical protection for critical infrastructure.

According to Chinese experts advising Zhongnanhai on Russian and Central Asian affairs, Beijing historically has been happy with the established division of labor with Moscow. Chinese attempts to forge bilateral security ties with countries of the region were seen as counterproductive since they could potentially jeopardize ties with Moscow or raise suspicions in local capitals about Chinese intentions. This line of thinking is slowly starting to change, as Beijing becomes increasingly worried about Moscow’s unpredictability, and also the Kremlin’s ability to maintain promised levels of investment in CSTO and its military installations in Central Asia.

Internal discussion on the role that China could play as a regional security provider are still in their infancy and rarely mentioned, if at all, in Chinese open sources.93However, according to Chinese academics, different ideas are being floated, such as establishing special Chinese private military companies or developing closer ties with regional armies. Notable recent developments include a March 2016 visit to Tajikistan and Afghanistan by Fang Fenghui, the chief of the PLA’s General Staff and a member of the Central Military Commission, to discuss bilateral military-to-military ties with both countries, as well as the establishment of a new security coordination mechanism for intelligence sharing and consultations among Beijing, Dushanbe, Kabul, and Islamabad. These developments have stirred anxiety in Moscow, with some experts labeling these moves an attempt to create an alternative, Beijing-centered security framework in the region that will put Russia at a disadvantage.94 Fang’s trip was also a topic for discussion between the Russian and Chinese envoys on issues pertaining to Afghanistan, Zamir Kabulov and Deng Xijun, during their March 2016 talks in Moscow.

The Kremlin’s official reaction to Beijing’s moves remains calm, as is seen in Kabulov’s remarks to the Russian government newspaper Izvestia.95 Nevertheless further Chinese attempts to boost its security role in Central Asia at the expense of Russia may erode fragile trust that has been fostered between the two countries’ national security establishments. Over time, such moves could undermine the overall relationship and, conceivably, trigger misunderstandings, miscalculations, and renewed feelings of geopolitical rivalry.

Toward Asymmetric Interdependence

Two years after Putin’s May 2014 visit to Shanghai, Russian hopes of a quick and stable Chinese alternative to European energy and capital markets are going through a painful reality check. Bilateral trade with China plunged by 28 percent in 2015 due to the fallout from lower commodity prices and the knock-on effects of the continued decline of the Russian economy and the devaluation of the ruble. Many of the Russian-Chinese deals inaugurated with much fanfare over the last twenty-four months have remained on paper. Leading Chinese banks have surprised the Kremlin with their rigorous adherence to Western sanctions. Capital markets in Shanghai and Hong Kong have remained largely closed to Russian issuers as well. The few existing channels of access to Chinese money through political banks remain open only for a handful of strategic state-owned companies and members of Putin’s inner circle.

Growing disillusionment with Moscow’s pivot to China is starting to come to the surface, aired in public forums by the most well-connected and wealthy Russian citizens.96 Similar disillusionment is widespread in Beijing, where officials and businesspeople complain about Russians being stubborn, arrogant, and short-sighted—missing a golden opportunity to open up to China as a result.

Still, temporary setbacks notwithstanding, Moscow and Beijing are drifting closer together. The fundamental conditions for Russian-Chinese rapprochement were present long before the Ukraine crisis. These include the complementary and increasingly interdependent nature of the two countries’ economies; a shared commitment to maintaining authoritarian political systems and limiting foreign influence at home, as well as to upholding principles of sovereignty and nonintervention in each other’s affairs; traditionalist social norms and values fueled by the great-power ambitions of large swathes of their populations; and a common elite and popular resentment of the West’s global dominance. The mutual distrust between the elites of both countries, particularly on the Russian side, and the very ambivalent personal stance of many powerful officials and tycoons in both countries toward the West, meant for many years that the two countries only saw marginal improvements in relations despite their many shared interests. Now the personal chemistry between Putin and Xi and the Western sanctions campaign against Russia have galvanized the partnership and may bring it to a new and higher level than before.

This new Russian-Chinese relationship may turn out to be more meaningful than previously was the case, but it is hard to overlook the degree of inequality between the two partners. The basic trend is one of Russia and China moving toward a deeper asymmetrical interdependence, with Beijing enjoying a far stronger position. The biggest new development is that this economic inequality may no longer be a barrier to greater cooperation. Russia faces continued estrangement from the West in the form of the sanctions regime, which will impact Moscow’s ability to build closer ties to U.S. allies such as Japan and South Korea. Russia lacks the political will to modernize its economy and institutions, which would require challenging various pillars of the current regime and vested interests. In that context, Moscow may be most comfortable with China as its key partner, especially as China is willing to accept Russia as it is. Beijing is, of course, unlikely to criticize Russia’s lack of progress on economic reforms or the poor state of its democracy. In return, Russia may become more accommodating on its terms for commercial cooperation with China.

If future gas and oil pipelines originating in Siberia end up leading to China only, Russia will deny itself options to branch out to other potential markets in other Asian economies via the Pacific Ocean. Gazprom’s suggestion that it may scrap the Vladivostok LNG project in favor of yet another pipeline to China suggests Moscow may already be moving in this direction. Before the Ukraine crisis, Russia was trying to create pipeline infrastructure leading to the Pacific Coast, while branch pipelines to China were seen as necessary preconditions for receiving Chinese funding (this was the case with the ESPO oil pipeline). Now, direct pipelines to China may become ends in themselves, particularly if commodity prices remain low and Russia continues to lack the technology it needs to build LNG plants.

A second major outcome could be Moscow’s acceptance of Chinese companies’ ownership of substantial stakes (including joint control with Russian minority stakeholders) in strategic deposits of natural resources. As remarks made by Russian Deputy Prime Minister Dvorkovich in Krasnoyarsk in 2015 show, this idea is already circulating within the Russian elite community. So far market conditions and hopes for a speedy removal from Western sanctions have allowed Russians to drive a hard bargain when discussing potential sales of these assets. However, if current conditions persist, Russia’s appetite for hard cash may grow in the medium term, and the Chinese may be able to buy assets at much cheaper prices. A third form of symbiosis could take the shape of joint ventures between Chinese companies and Russian businesspeople close to the Kremlin, in which the Chinese would provide technology and financing while the Russians would ensure Moscow’s approval of projects and bids.

Of course, if Western sanctions are eventually lifted or relaxed, commodity prices recover, or Russia embarks on meaningful structural reforms that dramatically improve its attractiveness to foreign investors, things could go back to their pre-Ukraine state. But all three of these scenarios seem rather far-fetched at the moment. Russia appears more likely to continue to slip further into China’s embrace, at least in the economic sphere. In this new scheme, the mutual benefits that both sides derive will compensate for the growing inequality between them. China will offer Moscow an economic lifeline, while Russia will provide vital resources (military and civilian technology, natural resources, and diplomatic support, including in the UN Security Council) to propel China’s rise as a global powerhouse that can compete with the United States. The bitter pill of Russia’s continued decline will be less painful amid Beijing’s efforts to show symbolic deference to Russia’s status as a great power. The tone of their official dialogue will differ sharply from what Moscow hears from Western interlocutors, as the values of the two regimes converge much more closely.