by Brad W. Setser

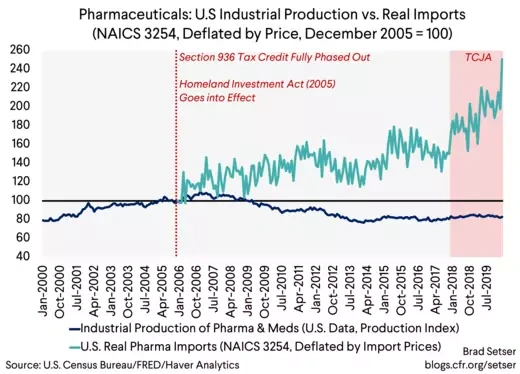

America’s production of pharmaceuticals and medicines peaked in 2006, back before the global financial crisis. Output now is about 20 percent below its 2006 level.

Pharmaceuticals tend to be capital not labor intensive. High quality pharmaceuticals aren’t made in sweat shops. Pharmaceuticals certainly weren’t the kind of industry that most economists expected to be on the losing end of trade liberalization twenty years ago.

Yet America’s consumption of pharmaceuticals didn’t peak in 2006. Only U.S. output. Imports have increased substantially since 2006.

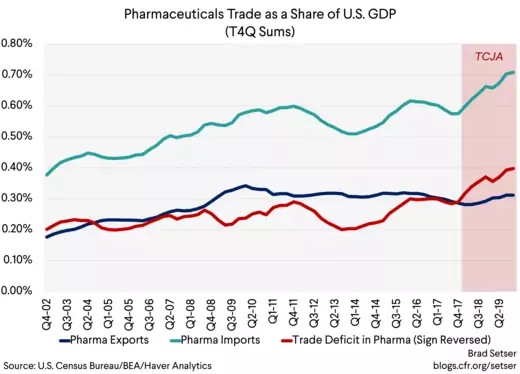

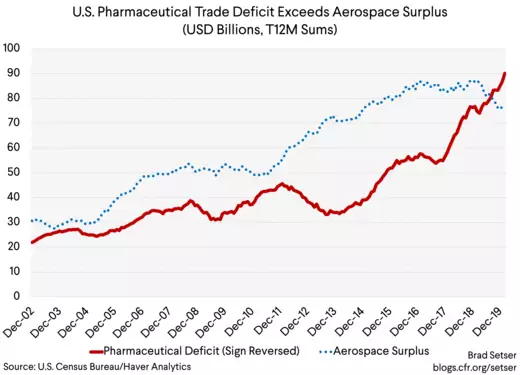

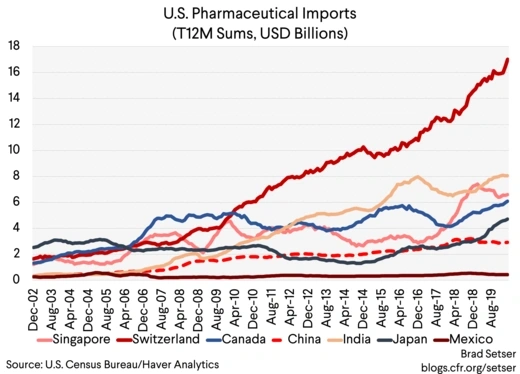

Imports of pharmaceuticals have increased from $65 billion in 2006 to $151 billion in 2019. As a result, the trade deficit in pharmaceuticals has increased from $32 billion at the end of 2006 to $93 billion in March of this year. That is about 0.4 percent of US GDP, or just under 10 percent of the total trade deficit in manufactures.

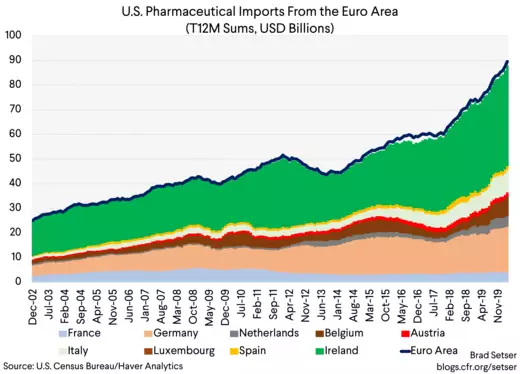

The bulk of these imports are from countries that pay high wages. The two biggest sources of imports are Ireland and Switzerland. Many of the usual arguments around the gains to consumers from trade don't really apply here. The imports are of patent protected goods, so they don't expand consumer choice. And U.S. pharmaceutical prices are notoriously high—imports from Ireland and Switzerland haven't brought U.S. pharmaceutical prices down to European levels. The bulk of the gains from trade here almost certainly go to the owners of the pharmaceutical companies who benefit from lower taxes. And the main loser is the U.S. Treasury. Right now, the United States pays the highest prices in the world for its medicines (many of which derive from NIH research) while U.S. pharmaceutical companies are often taxed at quite low effective rates.

Brad Setser tracks cross-border flows, with a bit of macroeconomics thrown in. 1-3 times weekly.

There has also been a particularly rapid increase in pharmaceutical imports and the pharmaceutical trade deficit in the last two years—after the Tax Cuts and Jobs Act.

Several major pharmaceutical companies have set up production lines for new patent protected high dollar pharmaceuticals in Ireland (Q1 Bulletin of the Bank of Ireland). This is exactly what critics of the international provisions of the Tax Cuts and Jobs Act predicted would happen at the time—as the provisions of the law encouraged offshore production of high margin products.

The government doesn’t put out a “real pharmaceutical imports” series to my knowledge—but pharmaceutical imports can be deflated by the price of pharmaceutical imports to get a rough idea of import volumes. They are up quite substantially over time.

The timing of the recent rise in imports suggest that it is is tied to incentives created by the Tax Cuts and Jobs Act. But what explains the inflection point in U.S. medical production back in 2005 and 2006?

Well, there are two overlapping explanations.

One is that the special 936 tax credits that made Puerto Rico a hub of pharmaceutical manufacturing were fully phased out by 2006. Of course, section 936 also made Puerto Rico a hub of legal tax avoidance—Microsoft was printing its floppy disks in Puerto Rico for some unknown reason (see ProPublica).

The other is that the Homeland Investment Act of 2005—which showed that firms could lobby hard and get a special window to repatriate tax deferred (i.e. largely untaxed) offshore profits at a special low rate—encouraged firms to aggressively shift profits abroad in anticipation of a new tax holiday. And with pharmaceuticals, the easiest way to shift profits abroad is to shift production abroad, and then play transfer pricing games.*

The U.S. tends to account for a majority of the sales of the big pharma companies, but they only report earning something like a quarter of their profit in the United States [pdf]. Tom Bergin and Kevin Drawbaugh of Reuters reported back in 2015:

"Pfizer has used transactions between companies within its group to allow an Irish subsidiary based in Ringaskiddy - Pfizer Ireland Pharmaceuticals - to buy the rights to patents developed in the United States and then use them to make drugs which are sold back to U.S. affiliates."

Most of the major U.S. pharmaceutical companies use variants on this strategy. Back in 2016, Jeremy Scott, the commentary editor-in-chief at Tax Analysts, noted: "People weren’t doing it as aggressively in the ‘90s as in the past five to 10 years ... This is a recent trend."

And while tax reform did change the legal structure of U.S. taxation of firms’ international profits, it didn’t actually do anything to reduce the incentive to offshore—rather the contrary. It certainly didn't raise the effective tax rate on many pharmaceutical firms.

Under the old tax system, the key incentive to offshore was the ability to defer (indefinitely) taxation on offshore profits. Firms stocked up big accounting profits abroad (the funds actually were always invested in U.S. bank deposits and U.S. bonds, so the funds themselves weren’t abroad—try finding a trillion dollars worth of assets to hold in Bermuda…) while waiting for a new Homeland Investment Act and on occasion borrowing against their offshore profits to move funds home.

The new tax law got rid of the old system of global taxation with indefinite deferral of tax on profits held abroad. There no longer is an incentive to build up offshore cash as a result.

But there continues to be a strong incentive to offshore actual production. In fact, the incentive to offshore production increased after the passage of the Tax Cuts and Jobs Act.

Profits tend to flow to the lowest rate in the tax code, and right now the lowest corporate tax rate is the 10.5 percent on global intangibles income.

A firm that wants offshore intangible income cannot easily produce goods in the United States for sale to the United States. Hence pharmaceutical firms appear to have an incentive to produce the most valuable pharmaceutical products offshore (after shifting the rights to some of their most valuable drugs to yet another offshore subsidiary to reduce their effective tax rate).**

The way the intangible income is calculated creates incentives to have tangible assets abroad (think factories) and firms can use taxes paid in say Germany to further reduce their intangibles tax but not taxes paid in the United States—so strangely the law even creates incentives in some cases to produce offshore in high tax jurisdictions rather than the United States.***

The details are complicated (see Kim Clausing or Rebecca Kysar or Lily Batchelder or more) but the effect of the tax cuts on pharmaceutical trade seem quite clear.

Perhaps the 2017 bill should have been named the “Tax Cuts and (Irish) Jobs Act” …

* Production costs are a small fraction of the price of a patented pharmaceutical. But if the drug is made in Ireland, the U.S. parent that markets the drug can pay a high price for the active ingredient to its Irish subsidiary, and in the process move its profit out of the United States. That is why the headquarters of many U.S. pharmaceutical companies historically lost money even though the overall group was profitable. A lack of any reported U.S. profit by a globally very profitable firm tends to be a strong signal of aggressive profit shifting. Pfizer is an extreme example. According to Americans for Tax Fairness: "Even though 43% of Pfizer’s sales were in the U.S. from 2007-16, its aggressive use of profit shifting allowed the company to report no taxable U.S. income over that entire decade." That is directly tied to Pfizer's manufacturing strategy. Bergin and Drawbaugh of Reuters: "Pfizer does have manufacturing plants in the United States but filings for its overseas units show non-U.S. companies supply over 80 percent of U.S. sales. Those sales generate margins of around 40 percent for Pfizer’s overseas arm - earning it over $17 billion in 2013. However, Pfizer has reported losses on its U.S. business in each of the past five years."

*** This could be solved by assessing the global intangibles low tax income (GILTI) tax on a country by country basis, as Gene Sperling has consistently noted. The countries that generate the bulk of U.S. imports here aren't a secret—and it isn't likely the companies are paying enough tax in the location of production to offset a country-by-country GILTI.

No comments:

Post a Comment